There's something 'animal' about the stock market right now

Stock prices continue to climb to new all-time highs even as expectations for earnings come down. These two opposing forces have caused valuations — as measured by the price/earnings (P/E) ratio — to get almost unreasonably expensive.

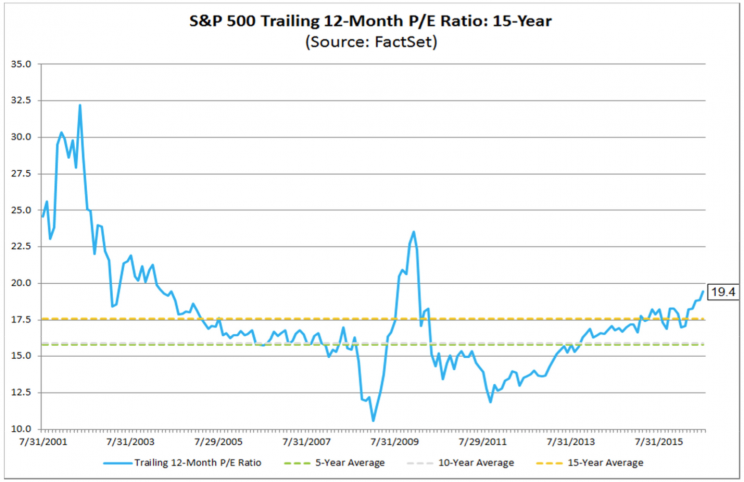

“The current trailing 12-month P/E ratio of 19.4 is above the three most recent historical averages: 5-year (15.8), 10- year (15.9), and 15-year (17.6),” FactSet’s John Butters observed. “Back on December 31, the trailing 12-month P/E ratio was 17.9. Since this date, the price of the S&P 500 (^GSPC) has increased by 5.9% (to 2163.75 from 2043.94), while the trailing 12-month EPS estimate has decreased by 2.5% (to $111.36 from $114.19). Thus, both the increase in the ‘P’ and the decrease in the ‘E’ have driven the increase in the trailing 12-month P/E ratio to 19.4 today from 17.9 at the start of the year.”

And as a result, it has become increasingly difficult for market bulls to justifying buying stocks using rational fundamental analysis.

Smells like ‘animal spirits’

RBC Capital Markets’ Jonathan Golub is among Wall Street strategists who have told clients that a high P/E ratio alone is no reason to sell. Apparently, that recommendation came with quite the backlash.

“In last week’s note, we laid out the case for higher multiples (favorable relative yields, generous return of capital, below average volatility) despite weaker earnings (slower GDP and trade, peaking margins),” Golub said in a note to clients on Monday. “Lesson learned … the only thing investors dislike more than a bearish argument is an optimistic one based solely on improving animal spirits rather than fundamentals.”

“Animal spirits” is a term popularized by economist John Maynard Keynes who used it to explain how emotions can drive behavior, more so than cold rational analysis.

Now, we can’t say with certainty that it is indeed animal spirits that are fueling this market. Indeed, numerous indicators of stock market sentiment would suggest the opposite. But, something is driving these prices higher, and animal spirits may explain at least some of why valuations will drift far from their long-term averages.

In a recent note to clients, Jefferies David Zervos suggested that central bankers helped ignite these animal spirits during the financial crisis with easy monetary policy. But he warned of the danger of these animal spirits getting carried away.

“When the economy enters a state like 2008–2009, some serious medicine is in order,” Zervos said. “With an unemployment rate of 10%, 9%, 8%, or even 7%, along with little evidence of future inflation risks, aggressive treatment is in order. That is a time for coddling, not for tough love. But as we approach 5% unemployment rates (and below), the mission has largely been accomplished. The game no longer requires the reviving of broken animal spirits. And if we keep pushing, as seems to be happening, the game will devolve – and animal spirits will rise to the point of frenzy. With many trophies on their shelves, players begin to believe they can’t possibly lose. So they start to do stupid things.”

Animal spirits can be a scary thing because they have the tendency to make markets swing too far in either direction.

“Similar to our clients, we are viscerally uncomfortable with the contradiction between soft fundamentals and rising valuations,” Golub said.

In other words, the head doesn’t feel good about what the heart is doing.

P/E ratios are not good at predicting the short-term.

This observation of animal spirits reminds us that we cannot use rational and fundamental measures alone to guide our investment decision, especially in the short-term.

“Empirical evidence shows that multiples are just as likely to rise, as they are to fall, during periods of decelerating earnings growth,” Golub added as he described the current situation.

If you look at the chart from FactSet above, you can see the P/E ratio drift in a way that doesn’t resemble the moves in stock prices or earnings during that same period.

BMO Capital Markets’ Brian Belski charted and wrote about this “befuddling” phenomenon in a note to clients on Friday.

“Valuation multiple expansion has been a key contributor to stock market performance over the past several years as earnings growth has decelerated,” Belski observed. “Yes, stock prices tend to follow earnings over longer periods of time, but for shorter horizons (one year), the picture is more complicated.”

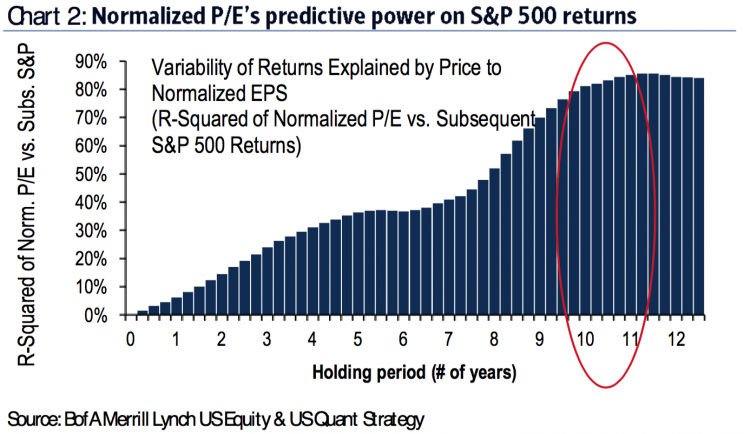

This is not to say the P/E ratios offer no insight as to what’s going on in the market and where it’s going. Indeed, when you account for inflation, P/E ratios are actually quite reasonable relative to historical averages. And as you can see from the chart below from Bank of America Merill Lynch’s Savita Subramanian, the predictive power of P/E ratios become more accurate when you lengthen your holding period; in other words, P/E ratios do a better job of telling you ten year returns than they do of one year returns.

“We don’t think anyone on earth can accurately forecast the market multiple in horizons less than several years (we believe we have done an effective job at proving this point),” Morgan Stanley’s Adam Parker wrote on Monday.

There are two takeaways from this discussion: 1) P/E ratios can measure value, but they won’t predict near-term price moves, and 2) animal spirits can cause prices to stretch valuations to points that are beyond rational.

Don’t kid yourself. Investing is hard.

–

Sam Ro is managing editor at Yahoo Finance.

Read more:

Everyone complaining about P/E ratios is using them wrong

Stocks today are reminiscent of 2 of history’s most exciting buying opportunities – RBC

The most important question in the stock market right now

The dumbest math mistake investors make in the stock market

Gutsy Wall Street analyst dares to debunk a sacred truism about the stock market