Yahoo Finance will host the exclusive live stream of Berkshire Hathaway’s shareholder meeting on May 6, 2017.

Berkshire Hathaway (BRK-A) (BRK-B) was a struggling textile company when Warren Buffett first invested in it in 1962.

Today, it’s a $400 billion behemoth. In Buffett’s own words, it’s a “sprawling conglomerate, constantly trying to sprawl further.”

The companies in Berkshire’s portfolio vary greatly. But one thing ties them all together: Buffett says they’re about “maximizing long-term capital growth.”

Here’s a brief introduction to Berkshire Hathaway.

The insurance business is the backbone of the company

After it acquired National Indemnity in 1967, Berkshire relied on its insurance businesses to power much of its expansion.

As Berkshire has gotten bigger and diversified its businesses, its insurance operations have become a smaller contributor to earnings than in the past, currently making up 26% of total company earnings. But they remain an important part of the company’s access to a permanent capital base by generating what’s known as “float.”

“Float” is money collected up front that is not paid out until later. In Berkshire’s property & casualty (P&C) insurance businesses, premiums are collected up front, but claims are paid out often years or decades later, allowing the float to be used for investments.

Today, Berkshire’s insurance group consists of four segments: GEICO (auto insurance), General Re (reinsurance), BH Reinsurance Group (retroactive reinsurance through subsidiaries), and BH Primary (focused on commercial markets, led by National Indemnity Co).

The property and casualty insurance business has faced headwinds—including deteriorating pricing and margin compression. But 2016 posted solid performance, with GEICO in particular making a comeback. Last year, GEICO suffered from higher personal auto claims (as a result of more low gas prices and more driving), and this year it accelerated new business efforts.

Berkshire’s insurance float was only $1.6 billion in 1990, and sat at $91.6 billion as of 2016. It is now over $100 billion, including the $10 billion reinsurance deal with AIG (AIG).

Equity portfolio

Berkshire’s investment portfolio represents Buffett’s long-term conviction ideas.

At the end of 2016, about 60% of his equity portfolio was invested in five companies—Wells Fargo (WFC), Coca-Cola (KO), IBM (IBM), American Express (AXP) and Apple (AAPL), a position he initiated last year and built up even more recently.

Buffett also made a big bet on airlines last year, diverging from his position in the past. He significantly increased his positions in Delta (DAL), United Airlines (UAL) and American Airlines (AAL) while adding a big stake in Southwest Air (LUV).

Shift to non-insurance businesses

Berkshire has evolved from its early years, when it was an insurance-driven company driven by outperformance on investments. It is now a large conglomerate that includes many non-insurance businesses.

The railroad business now comprises 22% of Berkshire earnings. Burlington Northern Santa Fe Railroad (BNSF), which Berkshire acquired in 2009 for $44 billion, is one of seven major railroads in North America and carries 17% of all inter-city freight. Berkshire has been investing heavily in this business.

Utilities businesses comprise 10% of Berkshire earnings. BH Energy owns four utilities servicing customers in 11 Western/Midwestern states, two electricity distribution companies in England, two interstate pipelines, a renewable energy business, and a residential real estate brokerage firm.

Berkshire’s manufacturing, service and retailing (MSR) operations, 35% of total earnings, include everything from candy to jets. Companies include food supply chain company McLane, manufacturing businesses (like specialty chemicals company Lubrizol, industrial components company Marmon, flooring company Shaw Industries, and paint and coatings company Benjamin Moore), service and retailing businesses (including NetJets, See’s Candies, Borsheim Jewelry Company, the Pampered Chef, and Oriental Trading Company), recently acquired battery maker Duracell, and aerospace components manufacturer Precision Castparts, which Berkshire bought in 2015 for $37 billion.

Its finance businesses, 8% of earnings, focus largely on the manufacturing and financing of homes and the leasing of transportation equipment. They include Clayton Homes, UTLX, XTRA, and other leasing and financing activities.

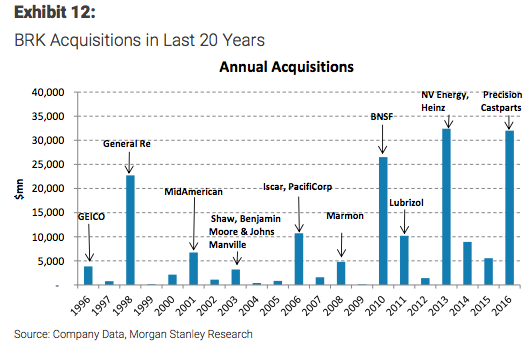

Acquisitions accounted for about 60% of Berkshire’s earnings growth in the past 20 years, according to Morgan Stanley.

As Morgan Stanley’s Kai Pan points out, Berkshire has a “managers as owners,” mentality, a decentralization that allows each unit to focus on long-term goals. Additionally, Pan highlights, each unit maintains an economic “moat” in its respective industry, separating it from competition to some degree.

More acquisitions are likely on the horizon for Berkshire, which has an estimated $60 billion in excess capital.

Valuation

Buffett’s preferred method for evaluating the attractiveness of investments and businesses is intrinsic value, which represents the sum of all of discounted cash flows that can be taken out of a business during its remaining life. The investor Whitney Tilson sees the current intrinsic value at $300,000 per share, significantly above the recent share price of $247,520.

Book value is another approach used to value Berkshire. However, Buffett has noted that the metric has underrepresented Berkshire’s intrinsic value because of the number of operating businesses Berkshire has acquired, which are held on the books at cost.

A book value calculation does, however, provide a floor for investors. Berkshire has an open-ended share repurchase program that authorizes management to repurchase shares if the stock price drops below a price-to-book ratio of 1.2x.

Beneficiary of stimulus

As Morgan Stanley’s Kai Pan points out, Berkshire has large exposure to Industrials and Financials and thus will be a major beneficiary of the administration’s “pro-growth” policies and tax reform, if they pan out.

“Given Berkshire’s outsized exposure in Industrials and Financials, it is not surprising that BRK shares have rallied +22% post-election vs. +14% for the S&P 500,” Pan wrote on March 20. “A potentially lower US corporate tax rate would also aid earnings. A 20% tax rate could boost BRK earnings by ~14% vs. its current ~30% consolidated tax rate,” he added.

The bottom line: Berkshire’s business has transformed over the years, but remains focused on long-term return and the efficient use of capital.

Nicole Sinclair is markets correspondent for Yahoo Finance

More about Warren Buffett and Berkshire Hathaway: