The Federal Reserve on Wednesday raised interest rates for the fourth time this year.

The Fed increased the target range for its benchmark interest rate by 25 basis points to a new band of 2.25%-2.5%, putting the Fed funds rate at its highest level since the spring of 2008. All ten voting members of the FOMC voted in favor of Wednesday’s decision.

In its statement, the Fed pointed to a labor market that has “continued to strengthen” and economic activity that is “rising at a strong rate.” The Fed did note the slowdown in private investment seen over the last several months, saying “business fixed investment has moderated from its rapid pace earlier in the year.”

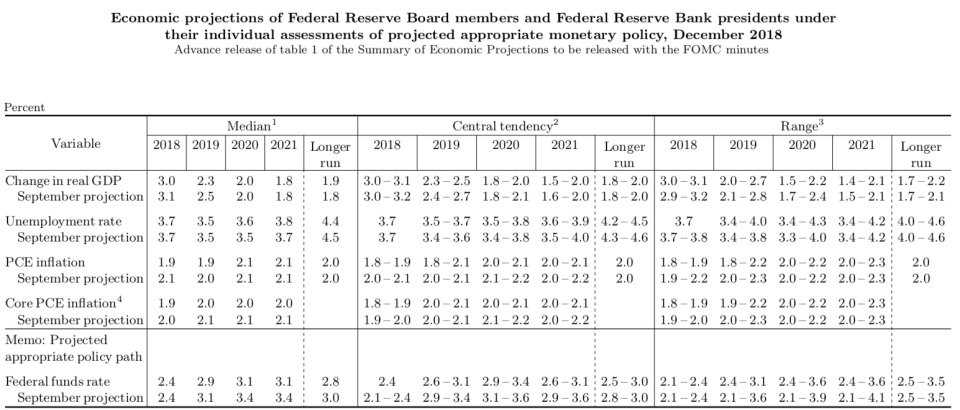

Along with its latest policy statement the Fed also released an updated set of economic projections, which shows a downgrade in the Fed’s forecast for interest rate hikes next year.

Fed signals fewer rate hikes for 2019

The Fed’s latest dot plot now shows the FOMC’s median forecast calling for two rate hikes in 2019, down from three in September. Six members of the FOMC, however, see three rate hikes next year as appropriate.

The longer-run neutral rate of interest that is expected to sustain full employment and price stability also fell slightly in December, with the median FOMC forecast now indicating the neutral rate is 2.8%, down from 3% in September.

In late November, Federal Reserve Chair Jerome Powell moved markets when he said the Fed funds rate was “just below” the range of estimates for the neutral rate of interest that allows the economy to sustain 2% inflation and full employment. That range of estimates has now come down, indicating the current cycle of interest rate increases is closer to its end than previously thought.

Ahead of Wednesday’s meeting markets had all but priced out any further rate increases in 2019. The Fed’s downgrade in its expected path for future rate hikes shows the central bank softening its view towards how many more interest rate increases will be needed before the neutral rate is reached, though market pricing and the Fed’s new forecast are still out of step.

Financial market volatility was also acknowledged by the Fed in Wednesday’s statement, with the central bank adding language which said it, “will continue to monitor global economic and financial developments and assess their implications for the economic outlook.” In November, the Fed said simply that risks to the economic outlook were roughly balanced.

The Fed made a key change to its forward guidance on Wednesday, saying that “some further gradual increases” in the Fed funds rate would be warranted. This alters previous language that had simply said “further gradual increases” would be necessary. The addition of the word “some” — in addition to the new dot plot — suggests the Fed is nearing what it sees as the end of the current tightening cycle.

Inflation forecasts downgraded

The Fed on Wednesday also tempered its expectations for economic growth this year and next, forecasting real GDP growth of 3% this year and 2.3% next year. In September, the Fed forecasted real GDP growth of 3.1% and 2.5% in 2018 and 2019, respectively.

Inflation forecasts for the Fed were also downgraded on Wednesday, with core PCE inflation now expected to rise 1.9% this year and 2% over the next three years. In September, the Fed had expected core inflation to rise 2% in 2018 and 2.1% in each of the next three years. Since the Fed’s September meeting, oil prices have declined sharply and inflation data have softened.

The Fed’s unemployment forecast was little-changed on Wednesday, with unemployment expected to be 3.7% this year and 3.5% next year, unchanged from September. In 2020 and 2021, the Fed now sees unemployment rates of 3.6% and 3.8%, respectively, increases of 0.1% from September’s forecast. Both years, however, are expected to see unemployment rates below the Fed’s long-run forecast of a 4.4% unemployment rate that sustains a “full employment” environment.

On a more technical note, the Federal Reserve also announced that the interest paid on excess reserves, or IOER rate, at 2.4%, 10 basis points below the upper band of the Fed funds rate.

In June and then in September, the Fed set the IOER 5 basis points below the Fed funds rate to maintain a cushion between the upper band of its targeted range and the effective rate paid out to reserves kept at the Fed. In recent months, the effective Fed funds rate has been sitting around 2.19%, just 1 basis point below the previous IOER.

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland