Why race to an IPO? Staying private may be more viable, study suggests

An initial public offering may no longer be the most attractive exit option for a high-growth startup.

That’s one of the key takeaways based on the results of Carta’s latest research, “The State of Private Company Financing in 2018,” released Tuesday based on a study of 6,627 primary financing rounds raised by 4,565 U.S.-based, venture-backed companies.

Cash raised and valuations for startups across rounds have taken a sharp turn higher this year, the equity management platform, which serves stakeholders at more than 10,000 companies including Slack, Coinbase and Trello, found in its report. And these factors, combined with smaller shares of late-stage companies being sold to investors, could provide an incentive for growth startups to stay private rather than search for capital on the public markets, which have seen increased volatility as of late.

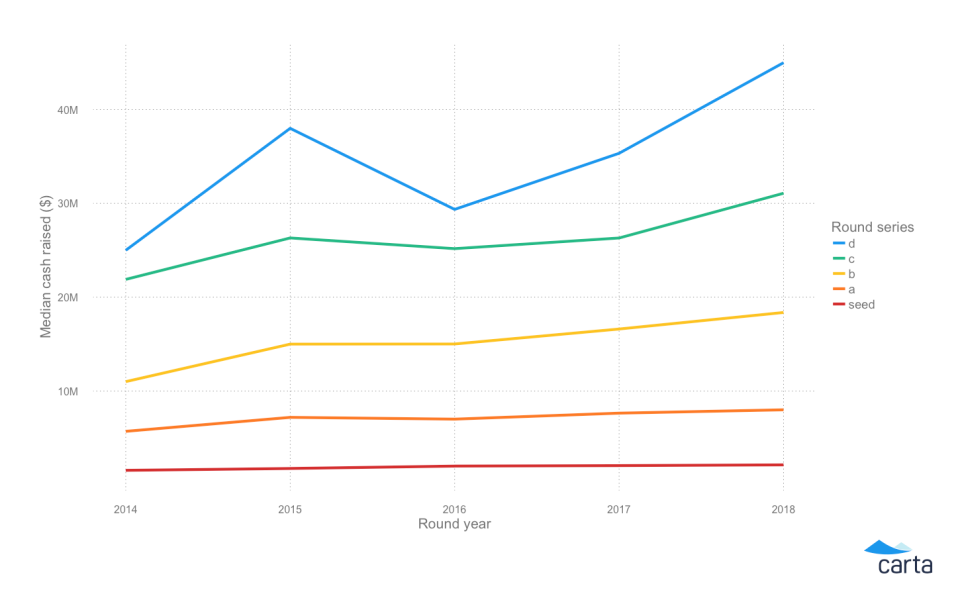

The findings were most pronounced for companies completing a Series D funding round, for which median cash raised increased by 27% to $45 million between the fourth quarter of 2017 and the third quarter of 2018.

But this hefty cash growth pales in comparison to the influx in startups’ median post-money valuations, meaning the value of a company after cash is raised, as calculated by price-per-share multiplied by a company’s fully diluted shares. Carta’s data found that median post-money valuations have risen across startups of all ages and exploded for late-stage enterprises, which are giving away less of their companies at skyrocketing valuations.

Post-money valuations have grown, on median, between 10% and 20% for seed through Series C funding rounds between 2017 and 2018. The median seed post-money valuation increased to $9.59 million from $8.5 million, while the median Series C post-money valuation increased to $165.6 million from $140 million. Seed funding is typically the first money invested in a company, while subsequent rounds of venture capital are typically used to help further develop products, scale up and offset a young company’s negative cash flow, and tend to be received in exchange for preferred stock options.

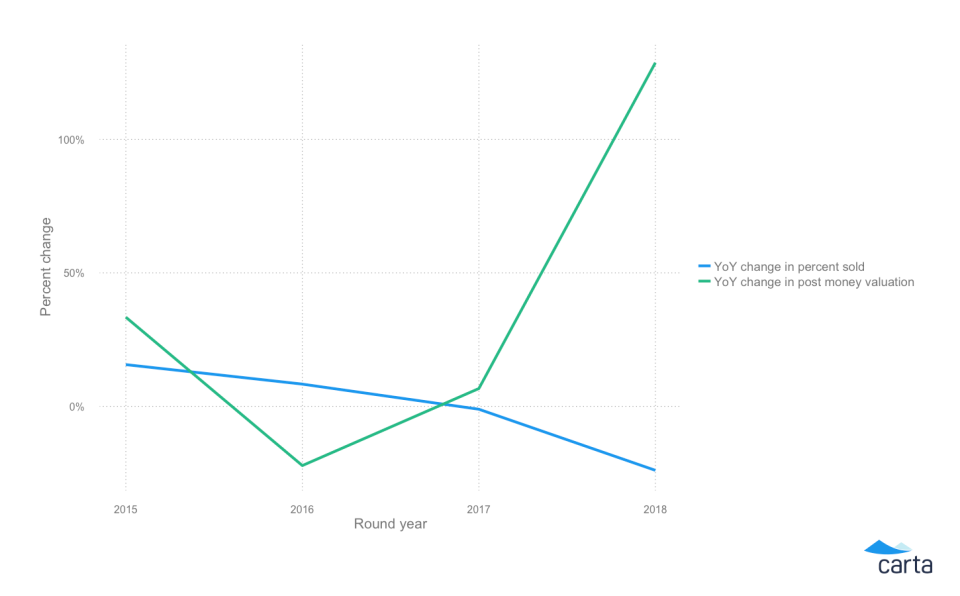

For Series D companies, median post-money valuations vaulted by nearly 130% this year, increasing to $420 million in 2018 from $183 million in 2017, according to Carta. But companies are retaining larger chunks of the pie after these rounds, with Series D rounds resulting in just 12% sold on median in 2018 from 17% sold in 2017.

‘Where companies go to die’

These interlocking phenomena mean that companies that manage to make it to the late stages of funding can then, quite literally, afford to stay private longer as financiers continue to provide ample liquidity. And that can present unique advantages, particularly when it comes to strategic investors, Carta CEO Henry Ward said in an interview with Yahoo Finance.

“Today going public is considered a win, it’s a goal in itself. I think tomorrow going public is where companies go to die,” Ward said. “They don’t have anything to innovate on, they don’t need capital anymore to invest and grow and innovate and build things for the future. They basically become cash flow engines.”

The findings are consistent with the investment strategies of some of today’s highest profile megafunds, which tend to back high-growth tech companies that delay going to public and raise larger sums of money to bring new products to market. These include the growth funds of the U.S.-based venture capital firm Sequoia Capital, as well as Masayoshi Son’s SoftBank Vision Fund, which has funneled billions across ventures including Uber, DoorDash, GM Cruise, Katerra, and Wag.

“It’s crazy to me that a public CEO doesn’t know who owns the company,” Ward said. “One of the reasons that a lot of innovation happens in the private world is because companies can pick investors that align with the mission and have a time horizon that matches the company. So you can invest in things that will take 8 to 10 years to come to fruition in the private world, where you just can’t do that in the public world.”

Ward said the rise of “growth investors” looking to target later-stage companies with high potential are partially behind the bloat of post-money valuations. A venture fund, for instance, might have $100 million earmarked for deployment and target ownership of 10% of a company, which would then imply a $1 billion valuation.

And indeed, the number of companies worth $1 billion – known in the startup community as “unicorns” – has swelled dramatically. Ward said about 100 companies with at least $1 billion are on Carta’s equity management platform, while CB Insights counts a total of 302 “unicorns” among startups worldwide. And consumer tech giants are not the only ones joining the club – companies from restaurant chain Sweetgreen to hiring service ZipRecruiter to enterprise product design platform InVision have all achieved proverbial unicorn status.

“The current trend that we’re seeing is that institutional money flows into venture in bigger amounts, they have to go into bigger funds, which means these funds have to find bigger companies to put them into. So valuations are skyrocketing for the late stages,” Ward said. “It’s a very good time right now to be a late-stage growth company.”

SpaceX model

While an initial public offering can unlock myriad benefits for companies – including increased public visibility and access to more liquidity – Ward isn’t convinced the exit strategy is meant for every enterprise. “The reason now to go public is somewhat vanity for the CEO and then liquidity for everyone else,” he said.

Instead, Ward envisions a future where companies implement private exchanges. This would provide sustainable access to liquidity as private investors and employees with corporate equity buy and sell shares of a company.

The model has already been established at companies such as Elon Musk’s SpaceX , which is not publicly traded but runs an exchange where private investors and employees have the option to buy shares or cash out.

And private companies also benefit from some insulation from market fluctuations, save for a macro-level recession, Ward noted. Companies completing IPOs this year through the first week of December have had shares leap 13% on average from IPO price to opening trade on public markets, Dealogic data found. However, companies listing after November 1 rose only 0.2%, or the weakest rate since November 2016.

Tech IPOs this year have especially borne the brunt of the recent market sell-off, and many investors who bet on tech companies go-public ambitions are now underwater in 2018. Companies including SVMK (SVMK), Spotify (SPOT), Sonos (SONO) and Domo (DOMO) all traded lower than their public debut prices as of market close Monday. And these flops create losses not only for outside investors, but also for the employees of the companies, who often forego high salaries for equity with the hope of capitalizing on upside as the companies grow.

“There’s this bubble around venture-backed companies where there’s so much dry powder waiting to get deployed even if the public markets crash or enter a downturn, they’ll still have so much money in the private venture world that it’ll keep things going for a while longer,” Ward said. “You don’t really care about the monthly, quarterly, annual volatility on the IPO market.”

—

Emily McCormick is a reporter for Yahoo Finance. Follow her on Twitter: @emily_mcck

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and reddit.

Read more from Emily:

Why the Huawei arrest is a huge problem for U.S.-China trade relations

Netflix user growth beats expectations, shares spike

Now is a ‘once-in-a-lifetime chance’ to invest in US pot companies, investor says

There are ‘4 headwinds’ facing markets rights now