Total U.S. household debt is now $993 billion higher than the peak of $12.68 trillion in the third quarter of 2008, according to a new report by the New York Fed.

According to the Fed’s Quarterly Report on Household Debt and Credit, household debt increased for the 19th consecutive quarter to $13.67 trillion and was “boosted by increases in mortgage, auto and student loan balances,” the report explained.

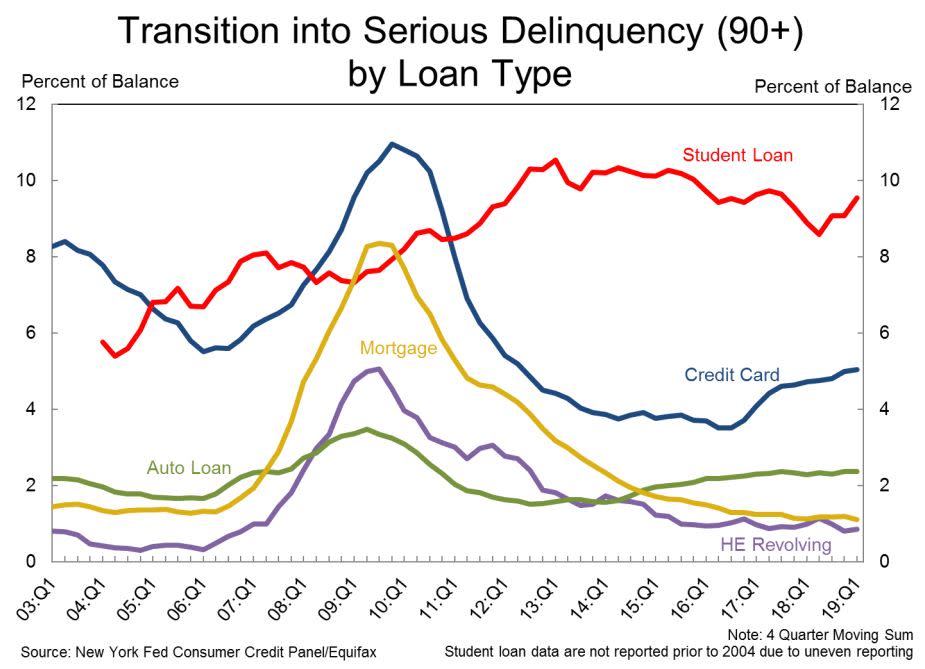

Serious delinquencies — payments that are late by 90 days or more — are also on the rise, driven by credit cards and student loans.

Auto loan delinquencies, which millennials struggle with, also rose slightly.

Deutsche Bank’s Torsten Slok said in a previous interview said that an increase in delinquency rates increases the likelihood of recession.

But not all economists agreed with the prognosis.

“We are not yet seeing signs of an inflection point in consumer credit cycle in the issuer performance data,” Fitch Ratings Senior Director, Non-Bank Financial Institutions Michael Taiano told Yahoo Finance. “What we are seeing reflects the seasoning of a resumption of consumer debt growth over the past few years after a period of stagnation following the financial crisis.”

Furthermore, added Taiano, “we anticipated some worsening in credit performance this year relative to last year when there were a number of macroeconomic tailwinds including the tax cuts. So it’s not that surprising to see some credit deterioration this year.”

Credit card delinquencies

Credit cards — the “most popular and common form of credit used by consumers,” according to the NY Fed — saw a worrying increase in the number of serious delinquencies.

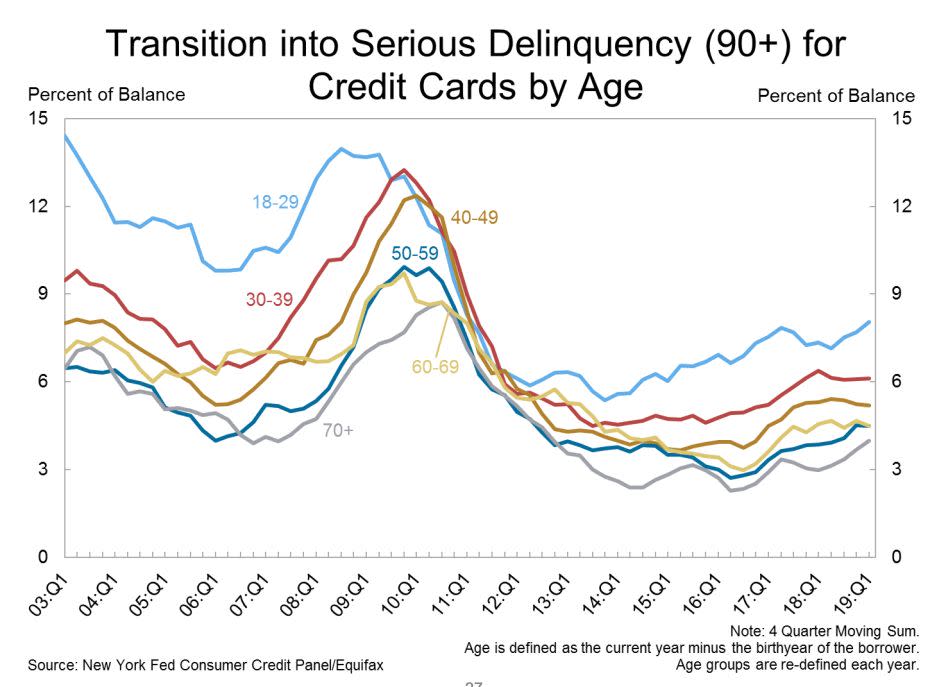

The 18 to 29 demographic in particular — Gen Z and late millennials — was finding it more difficult to repay credit card debt, as seen in the graph below.

“Credit card delinquency rates have been trending upward in the past few years — likely reflecting, in part, the increased presence of younger borrowers in the credit card market,” the report explained.

The trend is not an immediate cause for concern, the researchers added, because “despite this recent deterioration, credit card performance remains better than it was during the pre-Great Recession years of 2000-06.”

Student loan delinquencies

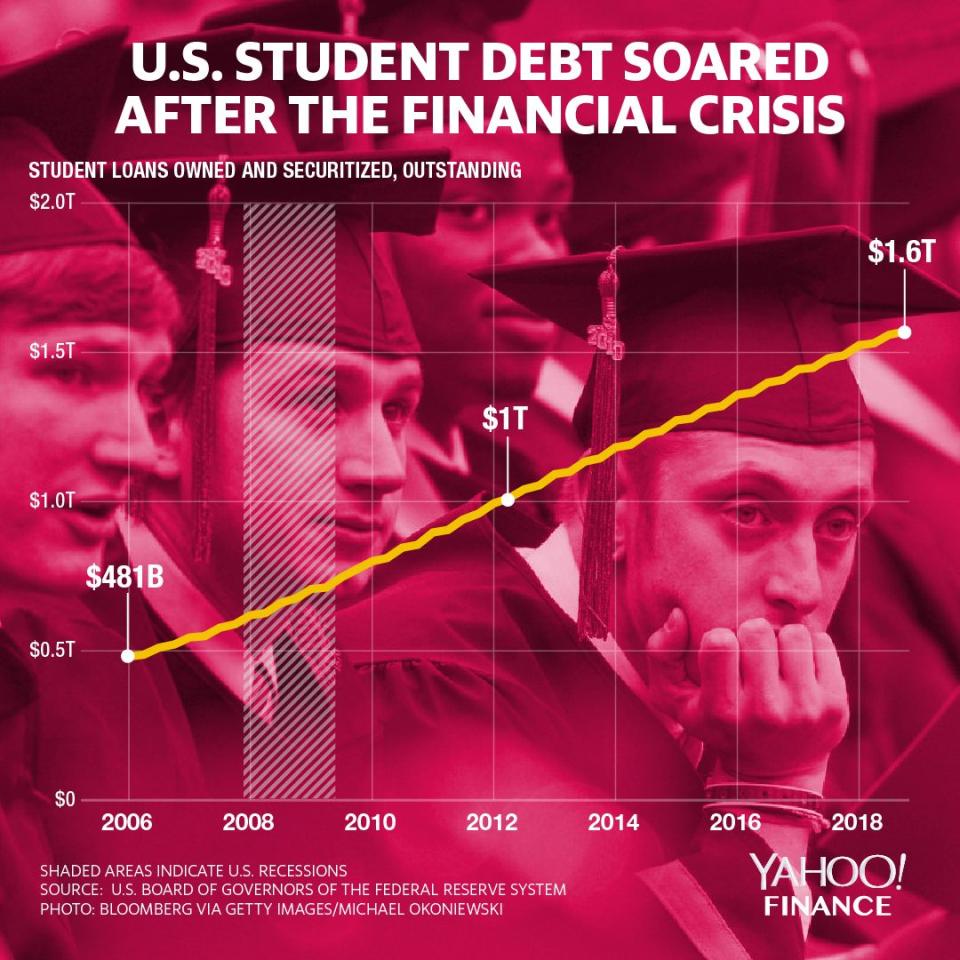

The percentage of student loans transitioning to delinquency — driven by borrowers unable to meet repayment deadlines — rose to 9.54% in the first quarter of 2019, up from 9.08% in the previous quarter.

And the number is likely to be understated, the Fed warned: “About half of these loans are currently in deferment, in grace periods or in forbearance and therefore temporarily not in the repayment cycle.”

Around 18% of the population has held student loans as of 2016, the report said, which was up from 10% in 2004.

The crisis has left millions of borrowers unable to achieve major life milestones like buying a house or getting married.

In a recent survey of 2,000 recent graduates by MidAmerica Nazarene University, the average loan amount was $25,893 which borrowers believed would take them 9.5 years to pay off.

Aarthi is a writer for Yahoo Finance. Follow her on Twitter @aarthiswami.

Read more:

Elizabeth Warren: 'Betsy DeVos is the worst Secretary of Education' ever

Elizabeth Warren unveils 'broad cancellation plan' for student debt

Dimon: U.S. student loan debt is ‘now starting to affect the economy’

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.