This post has been updated with comments by Senator Elizabeth Warren.

Total household debt overall grew by $92 billion in the third quarter to $13.95 trillion, according to new data from the New York Fed.

And while the overall debt pile for student debt increased in the last quarter — second only to mortgage balances — one group has been hit particularly hard: Black borrowers, who are on average borrowing more and defaulting at higher rates.

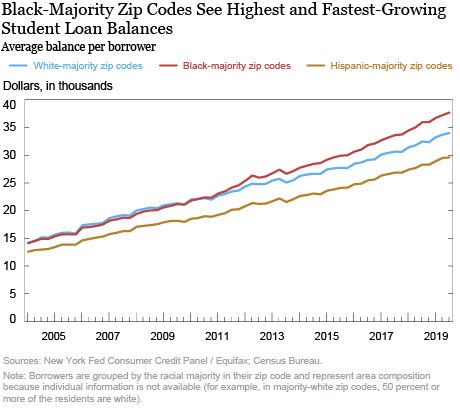

The average loan balance for borrowers in black-majority areas at the end of September was more than $37,000. That was “especially remarkable,” since the average income in these areas, according to the most recent data, was $38,000, the researchers remarked. It implied “very high debt-to-income ratios for student loans alone,” they added.

“Right now in America, African-Americans are more likely to borrow money to go to college, borrow more money while they're in college, and have a harder time paying that debt off after they get out,” presidential candidate Elizabeth Warren noted during the fifth debate on Wednesday. Drawing on a recently published study, she emphasized that the median debt of white student loan borrowers had reduced by 94%, 20 years after they started college, as compared to black borrowers who at the median still owed 95% of their total.

“I believe that means everyone on this stage should be embracing student loan debt forgiveness,” Warren added. “It will help close the black-white wealth gap. Let's do something tangible and real to make change in this country.”

Disparity in balances widening

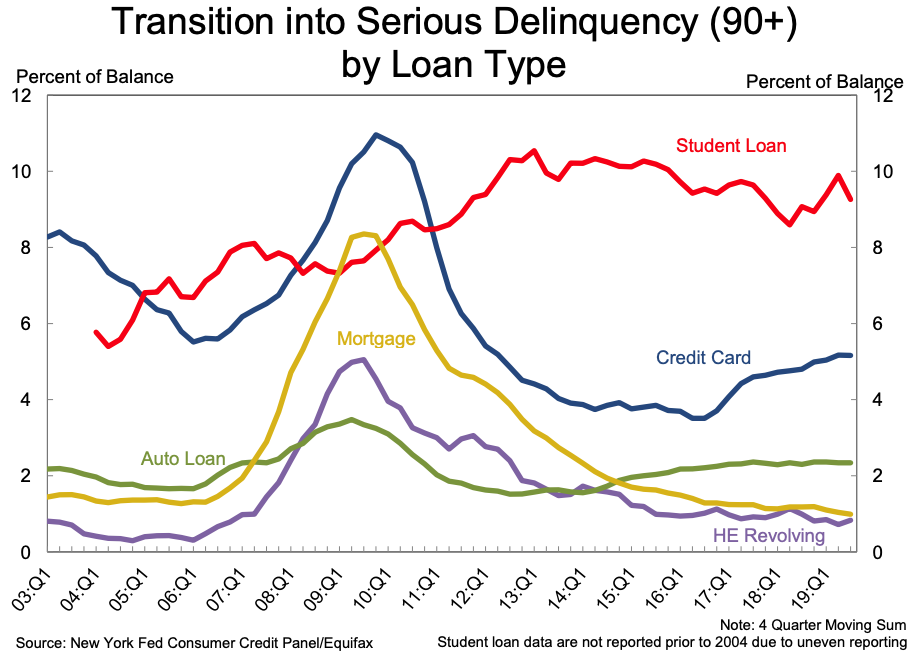

Outstanding student loans rose to $1.5 trillion — a $20 billion increase and a 1.4% growth from the previous quarter, according to the NY Fed. The data also determined that 11% of student debt was more than 90 days delinquent or in default in the last quarter.

Using data based on borrowers’ location and racial group from the U.S. Census Bureau’s American Community Survey, the researchers found that borrowers living in black-majority areas were the hardest hit by the student debt crisis in terms of carrying heavy balances and defaulting on loans.

“Borrowing rates are somewhat higher in areas with a majority of black residents” at 23%, the researchers wrote. In contrast, Hispanic-majority zip codes saw borrowing rates at 17% while white-majority zip codes borrowed at 14%.

The difference in borrowing rates is “likely explained, in part, by income disparities, as lower-income students are more likely to need student loans to afford tuition, even with need-based aid covering some of the affordability gap,” the researchers stated.

And the disparities carried over into loan balances. The growth rate of student loan balances, as seen in the graphic below, has also been diverging steadily since 2010 as borrowers in black-majority zip codes started borrowing more than white-majority and Hispanic-majority zip codes.

Default rates

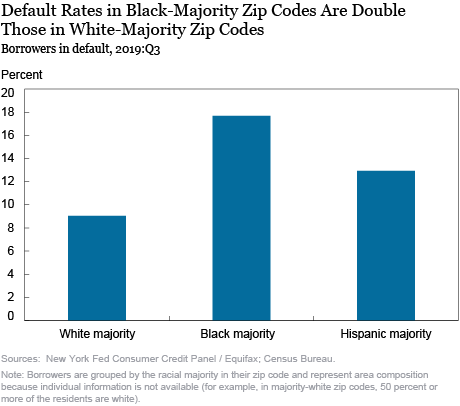

The growth in balances and high debt-to-income ratio affected default rates, as seen in the chart below. The Fed’s research shows that default rates were much higher in black-majority areas, at 17.7%, as compared to 9% in white-majority areas.

“The repayment struggles suggested by relatively higher default rates in majority-black and majority-Hispanic areas point to the likely importance of income differences across borrowers from different areas,” the researchers stated.

“With default rates that are almost at twice the level of those students who live in predominantly white neighborhoods, we can see that these debt figures underscore a story that mirrors much of what is going on in the broader economy,” Tally’s personal finance expert, Manisha Thakor, told Yahoo Finance in an email interview. “When it comes to income disparity and personal finance struggles, all men are NOT created equal.”

A recent study by the American Council on Education noted that one of the big factors for African Americans’ large student debt load — particularly for graduate students — was that they disproportionately enrolled in for-profit institutions, rather than public or nonprofit colleges, no matter their degree type.

When they earned their doctoral degree at these institutions, they ended up with more than $128,000 in student debt.

—

Aarthi is a writer for Yahoo Finance. She can be reached at aarthi@yahoofinance.com. Follow her on Twitter @aarthiswami.

Read more:

Republican student loan official who quit: The current system is 'an abomination'

'Severely derogatory': U.S. student debt defaults have 'grown stunningly'

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.