Friday, May 1, 2020

Get the Morning Brief sent directly to your inbox every Monday to Friday by 6:30 a.m. ET. Subscribe

April baffled investors from start to finish

April 2020 lived up to its billing — it was indeed the cruelest month.

When April began, the number of confirmed COVID-19 cases in the U.S. totaled 215,177. By month’s end, more than 1.06 million cases had been confirmed.

The death toll in the country has topped 60,000; on April 1, fewer than 5,000 COVID-related deaths had been recorded. Bodies are piling up outside funeral homes in New York. Experts believe COVID-related deaths in the U.S. have been severely undercounted.

Job losses have been staggering. In the past four weeks more than 20 million Americans have filed for unemployment insurance. Next week’s jobs report is expected to show the unemployment rate climbing into the double-digits in April.

GDP data published Wednesday showed the first quarter marked the biggest contraction in economic growth since 2008. The second quarter will be worse. In April, the price of oil went negative and the IMF coined a startling new term to describe our economic moment — The Great Lockdown.

And all the while stocks rallied aggressively.

The Dow rallied some 10.5% in April, to log its best April performance since 1938. The S&P 500 gained more than 12% and enjoyed its best month since January 1987. The Nasdaq gained the most since April 2001.

And while whether the stock market is a good representation of the broader economy is an eternal debate in the business world, April’s judgment was clear: stocks did not reflect April’s lived experience.

Of course, the job of financial markets is not to assess the present but discount the future. Investors are focused not on realized but anticipated changes in the economy, on whether things will get better or get worse from here.

As we wrote last week, some experts are seeing signs that economic data will not likely get worse from here. Comments from corporate executives this week also suggested as much.

Facebook (FB) CFO David Wehner said Wednesday, “After an initial steep decrease in ad revenue in March, we have seen signs of stability reflected in the first 3 weeks of April. Ad revenue has been approximately flat compared to the same period a year ago.” On Thursday, Apple (AAPL) CEO Tim Cook told Bloomberg TV that sales started to “pick up” in the second half of April.

Skeptics, of course, are not in short supply. A near consensus view among investors has been that the March 23 lows will eventually be re-tested. And indeed they may.

But at least in April the old adage that the market will try to make fools of the largest possible number of participants held true.

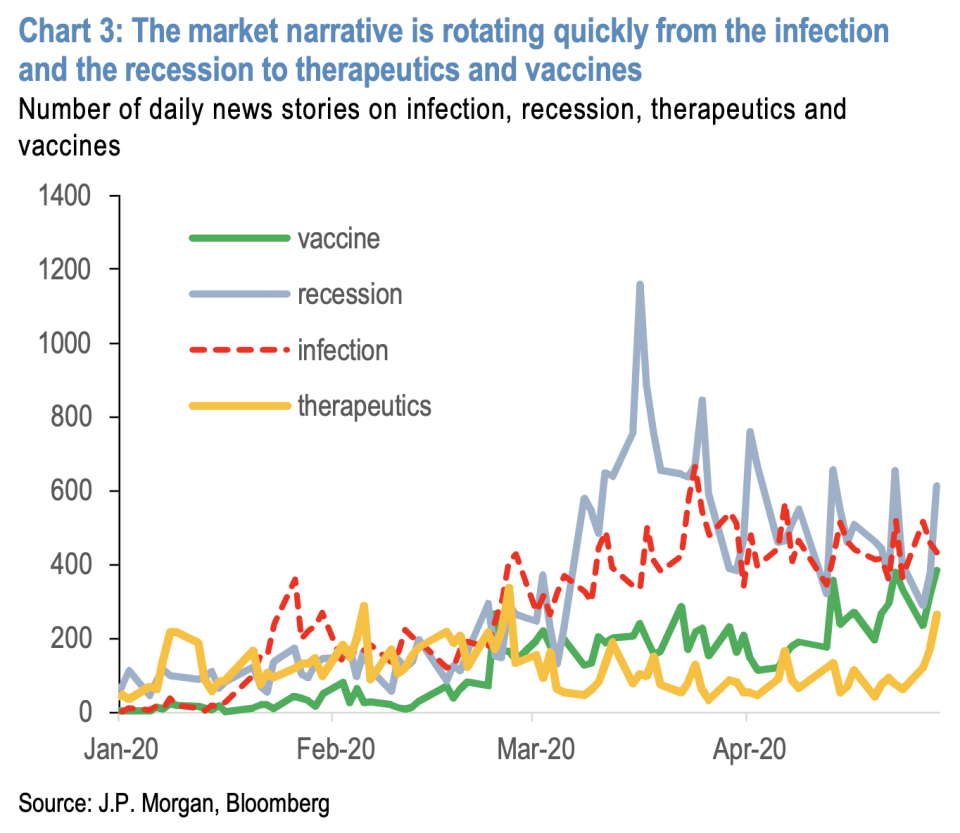

In the months ahead, the most important variable for investors will be containment of the spread of the coronavirus and progress on potential treatments or a vaccine. As JPMorgan’s John Normand outlined in a note published Thursday, the market’s emerging dominant narrative is “starting to latch onto rapid development of COVID-19 therapeutics and hopes for a vaccine, and therefore fewer public health risks to reopening economies and a quicker return to normalcy.”

“This evolving theme is already evident in the news flow, which has been flat-lining throughout April for topics like infections and recession, while accelerating around topics like therapeutics and vaccines,” Normand adds.

Re-opening economies, of course, remains a fraught endeavor. Strategists at UBS earlier this week said they expect stocks would fall below their March 23 lows if lockdown restrictions being lifted now are reinstated later this year on account of a renewed spread of the virus.

And as the equity derivatives team at Bank of America Global Research wrote earlier this week, “history suggests it would be highly unlikely for the S&P not to re-test its [March 23] lows given both the size of its recent drawdown and the fact a recession is underway.

The firm asks, however, if the four most dangerous words in investing may indeed apply.

“However,” BofA strategists write, “the speed of the recent bear rally on the back of record and rapid policy stimulus has some wondering if this time is different?”

By Myles Udland, reporter and co-anchor of The Final Round. Follow him at @MylesUdland

What to watch today

Economy

10 a.m. ET: ISM Manufacturing activity April (expected 37.0, compared to 49.1 in March); ISM New Orders April (expected 30, compared to 42.2 in March); ISM Prices Paid April (expected 33, compared to 37.4 in March); ISM Employment April (43.8 in March)

Earnings

Pre-market

7:30 a.m. ET: Exxon (XOM) is expected to report earnings of under 1 cent on $50.83 billion in revenue

8:30 a.m. ET: Chevron (CVX) is expected to report adjusted earnings of 66 cents per share on $31.10 billion in revenue.

Top News

Markets fall as Trump threatens China tariffs over pandemic [Yahoo Finance UK]

Amazon posts higher 1Q sales on coronavirus-driven spending, sees $4B in 2Q costs [Yahoo Finance]

Apple Q2 earnings rise on App Store, Apple TV [Yahoo Finance]

Boeing raises $25 billion from bonds, will no longer seek federal aid [Reuters]

YAHOO FINANCE HIGHLIGHTS

The risk for markets if Biden beats Trump

These workers lived in a factory 24/7 for 28 days to fight coronavirus

Kellogg CEO: 'People are eating more of our cereal'

—

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.

Find live stock market quotes and the latest business and finance news

For tutorials and information on investing and trading stocks, check out Cashay