2016 was an eventful year in the stock market.

The year began with the worst start on record as vague fears over economic growth in China had markets on edge.

Then June’s surprising Brexit vote sent stocks tumbling, drove the British pound to a generational low and had interest rates plummeting to record lows around the world.

And then came the US election, which also surprised markets and sent US stocks initially lower before igniting the “Trump rally” into year-end.

When the dust settled, the S&P 500 finished the year up about 10%.

The Dow Jones Industrial Average gained about 14%.

And while news headlines won’t allow 2016 to be a year many of us forget soon, the year for investors might be memorable if only because the main lesson learned was the oldest one in the book: Stay calm, and stay invested.

Telling — or reminding — investors that time in the market is more important than timing the market is standard-issue advice. It is, perhaps, the most common piece of investing wisdom passed along by financial advisors and the media.

Rarely do investors, and even those who preach this lesson, get such a vivid run of examples on why this advice has been so tried and true: 2016 was full of such moments.

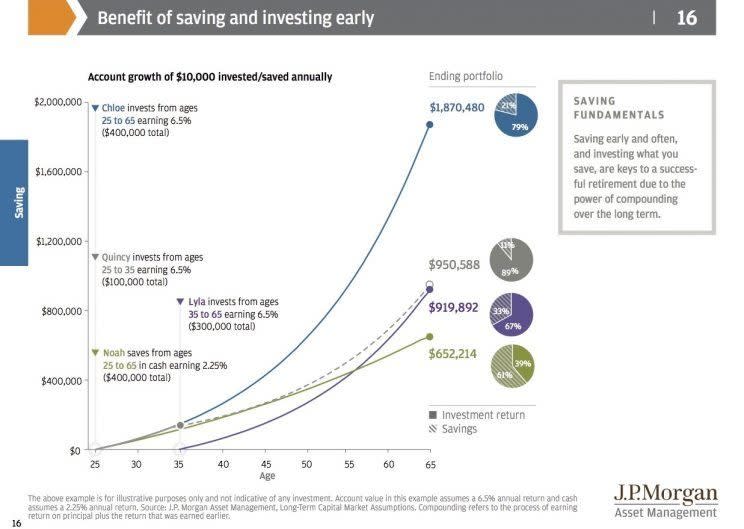

A chart we like to reference from time to time is one our managing editor Sam Ro once said every 25-year-old in America needs to see. And this is still true.

As this chart shows, the benefits of retirement savings accrue most dramatically to the saver who has spent the most time investing, plain and simple.

But while the lines on this chart seem to arc up and to the right, as we learned from 2016 news stories, political shifts and sentiment changes can often make the road to higher returns a perilous one. But in these cases, time is your best — and perhaps only — friend.

“Investors often think they should move in and out of financial markets, trying to time the buying/selling of stocks based on a series of events or increasing/decreasing their bond exposure depending on expectations for interest rates,” Bank of America Merrill Lynch strategists Martin Mauro and Cheryl Rowan wrote in a note to clients earlier this year.

“History shows the value of staying invested in bonds for the income generated regardless of rates and proves the rewards of staying invested in stocks despite periodic market declines.”

In their note, Mauro and Rowan included the following table, which shows returns on the S&P 500 when leaving out the 10 best days per decade.

And while it may seem crazy that just 10 days over a 10-year period would have such a dramatic impact on returns, the reason we preach time in the market as the key to success is because time allows the effects of compounding interest to really take hold.

In recent days, the hubbub in markets has been about whether or not the Dow would crack 20,000. Whether the index does so tomorrow or next year or in 2018 doesn’t really matter. The Dow will eventually trade to 20,000, just as it will trade to 25,000 and 30,000 and 40,000, given enough time.

And while these numbers may seem dramatically high, consider that the Dow going to 40,000 from 20,000 is the same as the jump from 5,000 to 10,000 on a percentage basis. It is only that the starting level of the index — 20,000 vs. 5,000 — is higher now. We’re still talking about a doubling of the index, something that has happened before and will happen again.

Over the last century, the Dow has averaged a 7.27% annual return. If the Dow starts 2017 at 20,000 on the dot, it will close at 21,454—if history holds. If it does that in each of the next two years, we’ll be knocking on the door of Dow 25,000 (24,687, to be more exact) by the end of the decade.

The disciplined investor that isn’t scared off by news headlines, political developments, or moments of self-doubt and fear will stand to capture the benefits of hanging in there and staying invested, through thick and thin.

Just like those who hung tight in 2016.

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland

Read more from Myles: